Table Evidence

The Excel add-in sends entity-scoped workbook tables into CORE as versioned, reviewed evidence staged for underwriting.

§ Platform - Underwriting Workspace

The underwriting workspace is where confirmed spreads, table evidence, scenarios, capital stack, coverage, policy tests, risk themes, waivers, and memo treatment meet in one borrower file.

CORE measures the file against the tenant's own credit box: policy tests, coverage periods, scorecard factors, covenant applicability, waivers, compensating factors, and memo treatment. The policy snapshot, inputs, exceptions, and sign-off stay attached to the project history.

Bound policy, coverage, and risk treatment in one file§ Judgment Layer

The Excel add-in sends entity-scoped workbook tables into CORE as versioned, reviewed evidence staged for underwriting.

Lender base, borrower base, and downside cases carry assumptions, projections, and sensitivity context without becoming disconnected spreadsheets.

Facilities, guarantee splits, debt service, rate shocks, and sources-and-uses stay inside the underwriting record.

DSCR and related tests are measured by the bound policy and period lens, with source context visible when a number is missing.

Risk themes become decisions: carry as risk, accept mitigant, require condition, require diligence, or exclude from memo treatment with rationale.

Waivers, compensating factors, scorecard factors, and sign-off are saved with policy version, inputs, and recorded-by history.

§ Fit

The page is for the judgment work competitors flatten into a status column.

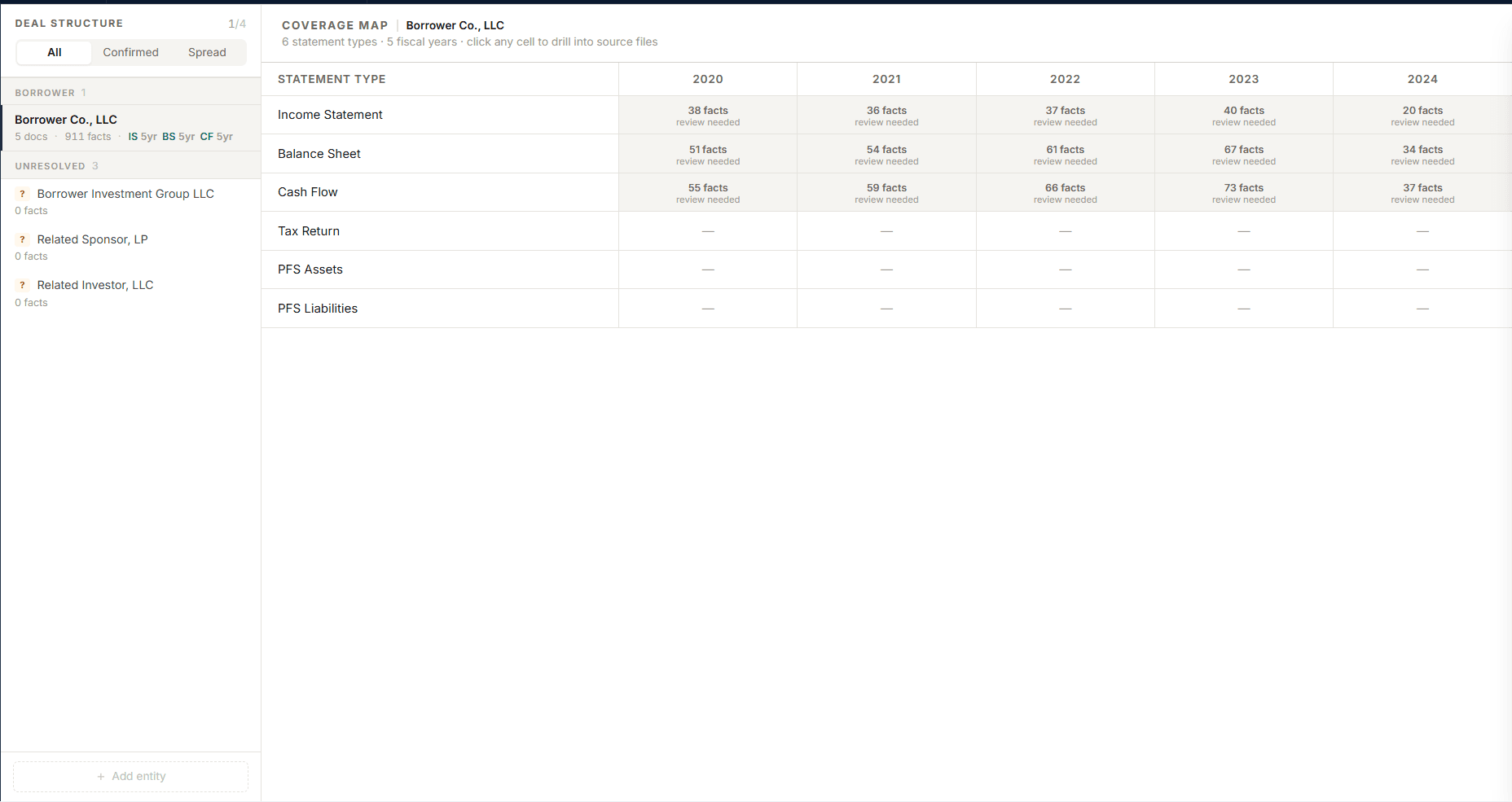

Workbook-sourced Table Evidence and AppSource Excel add-in path

Historical spreads and confirmed metrics feeding policy

Scenario pro forma and sensitivity context

Guarantee-aware capital stack and debt-service math

Coverage, policy tests, covenant applicability, and scorecard factors

Risk themes that land as memo decisions with waiver/sign-off history

§ Path

Spreads and table evidence are reviewed before policy tests can rely on them.

The program's policy snapshot defines thresholds, scorecard factors, covenants, and waiver rules.

Themes, exceptions, conditions, and mitigants are decided by the analyst instead of rediscovered in the memo.

Memo generation consumes the signed-off risk and policy state; it cannot recalculate around the decision.

§ Next Step

We will walk through how CORE keeps policy, projections, risk, waivers, and memo treatment attached to the same borrower file.