§ The four sections that earn the report

Where COREView differs from a market-research report.

Most industry reports explain the market. COREView frames the credit decision: lendability, structure, covenants, watchpoints, and post-close monitoring.

02

Credit & Lending Summary

The first read for a credit analyst: industry risk, lending posture, and the terms to consider before opening the memo.

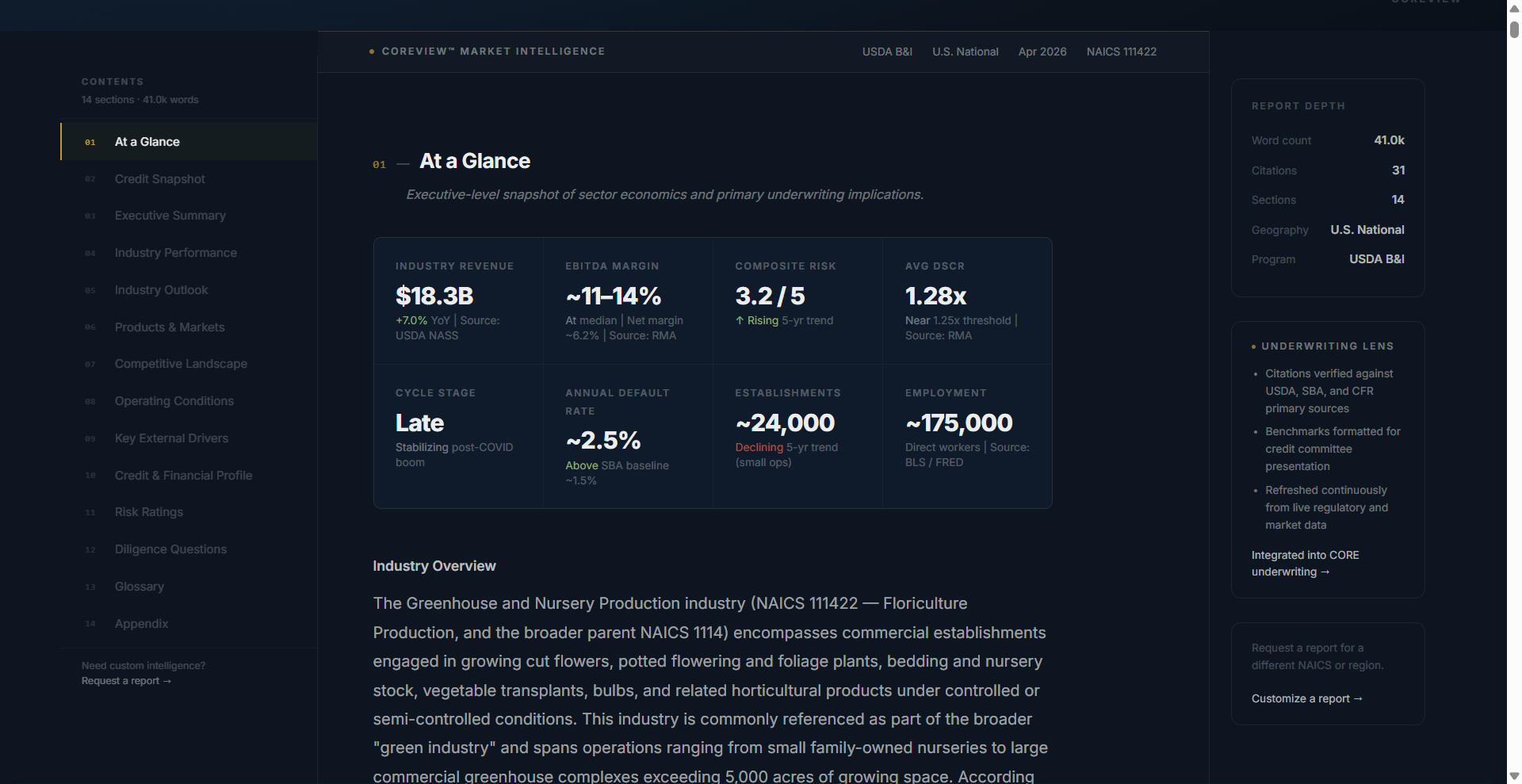

- Credit risk classification with justification

- Lifecycle and credit-cycle position with evidence

- DSCR, leverage, interest coverage, and working-capital ranges

- Typical loan structures, terms, collateral, and advance rates

- Top underwriting watchpoints and key success factors

10

Credit & Financial Profile

The quantitative section that maps directly to spread review, covenant design, and credit-committee discussion.

- Cost structure and revenue segmentation

- Strong / Acceptable / Watch thresholds for core credit metrics

- DSCR, fixed-charge coverage, and working-capital cycle ranges

- Multi-variable stress scenarios tied to covenant breach risk

- Recommended covenant levels transferable to the memo

11

Industry Risk Ratings

A 10-dimension risk score built for credit review, not a subjective Low / Medium / High graphic.

- Revenue volatility, margin stability, and capital intensity

- Competitive intensity, regulatory burden, and cyclicality

- Technology, concentration, supply-chain, and labor sensitivity

- Weighted composite score on a severity-banded chart

12

Diligence Questions & Considerations

The questions a lender should ask before approving, sizing, or monitoring an exposure in the sector.

- Revenue quality, margin durability, and DSCR history

- Debt history, covenant compliance, and prior restructurings

- Capacity, key person risk, customer concentration, and pricing power

- Regulatory exposure and industry-specific watchpoints

- Monitoring triggers for post-close portfolio review