Relationship-rich borrowers

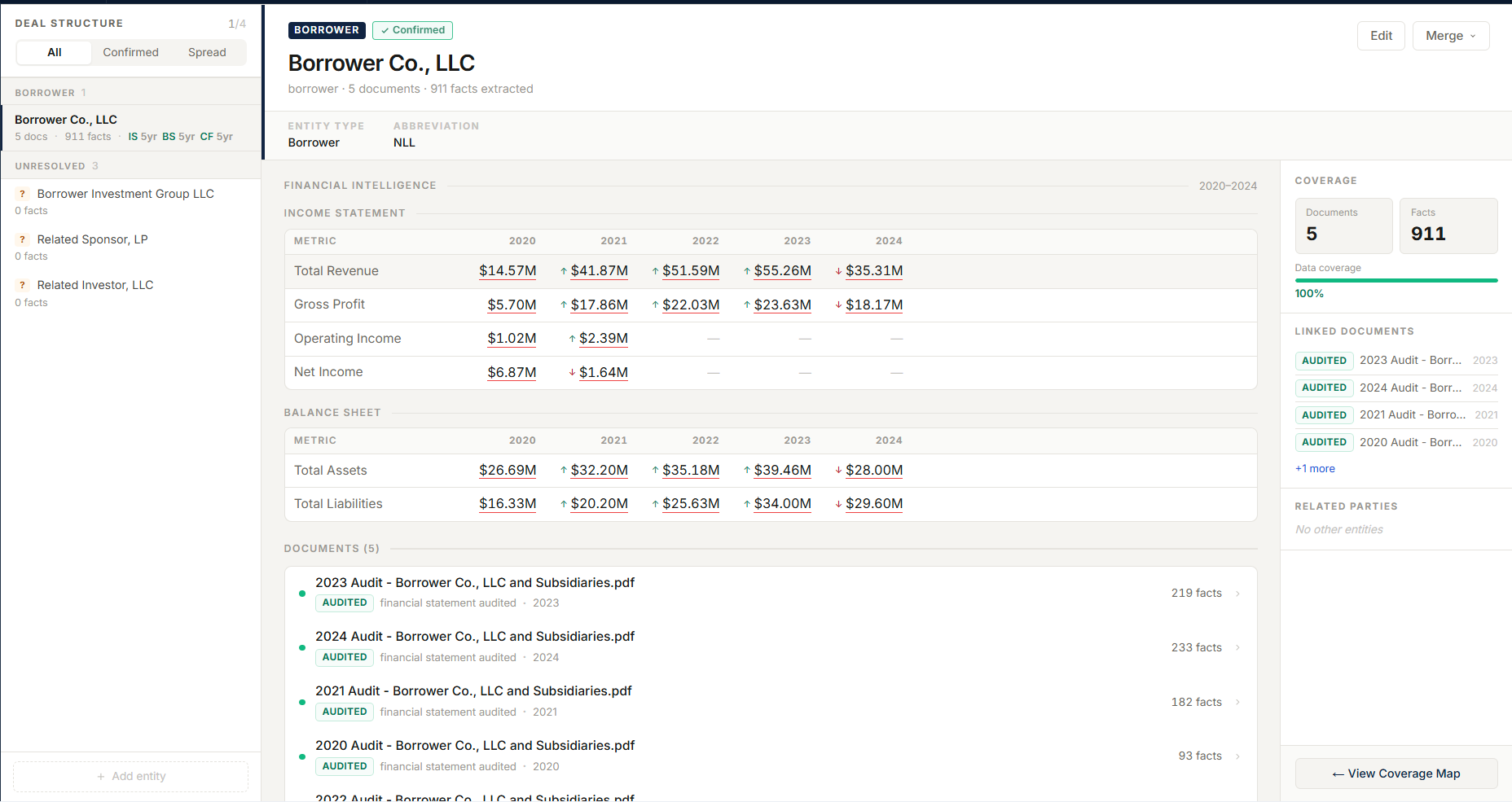

The credit story spans operations, ownership, related parties, repayment capacity, collateral, and member context.

§ Who We Serve - Farm Credit

Farm Credit teams know the borrower better than any generic system will. CORE is for the discipline around that relationship: financial evidence, collateral support, policy review, analyst judgment, and the record that explains the decision later.

CORE keeps borrower financial evidence, multi-year spreads, related-party facts, collateral support, policy context, analyst decisions, and source documents in the same controlled file. Association credit standards live as your own underwriting policy in CORE - your metrics, your covenants, your scorecard - versioned and cited when they shape memo language.

Entity profile with financial intelligence and policy context§ Association Credit

The credit story spans operations, ownership, related parties, repayment capacity, collateral, and member context.

Spreads, facts, exceptions, and analyst adjustments should resolve back to the audit, tax return, statement, or source table.

Credit standards, association policy, and relevant regulatory material should be versioned and cited when they shape memo language.

Generated recommendations stay separate from the analyst decision, supervisor review, and final accepted record.

Appraisals, liens, insurance, environmental support, and valuation notes belong in the same file as the repayment story.

When an FCA, internal, or board question comes back, the team should not rebuild the evidence trail by hand.

§ Fit

Best for associations that want AI assistance around the file without weakening credit discipline.

Borrower, guarantor, affiliate, and related-party entity review

Historical spreading with source-linked financial facts and analyst adjustments

Collateral, insurance, appraisal, and environmental evidence organization

Policy-aware memo support with analyst and supervisor control

Dated regulatory and credit-policy context for source-cited claims

Audit history for generated, accepted, edited, and rejected work

§ Path

Pick a credit segment where documents, spreading, collateral review, and memo pressure are visible.

Align entity types, source documents, financial periods, collateral evidence, and review stages to association workflow.

Compare CORE against the current analyst process before expanding the workflow.

Review source spans, analyst decisions, supervisor actions, and replayable audit history before broader rollout.

§ In Depth

Association structures, patronage context, and FCA examination posture shape how Farm Credit files must read. CORE keeps the borrower file, policy state, analyst actions, and audit trail together so the record satisfies the examination standard as a byproduct of doing the work.

Commodity cycles, operation-type economics, and regional conditions are not context for an ag file — they are the analysis. Cited industry intelligence belongs inside the credit work, feeding benchmarks and risk discussion rather than sitting in a separate research folder.

A working farm operation is routinely a web of operating companies, land-holding LLCs, family guarantors, and related entities. CORE assembles that structure as reviewable context and keeps every financial fact attached to the right entity — the difference between a consolidated story and a defensible one.

§ Next Step

We will show how CORE keeps the relationship story, source facts, and credit decision traceable.