For CDCs · Farm Credit · USDA · HUD · EB-5 · C-PACE · CDFI · Private Credit

The configurable underwriting engine built inside an active credit operator.

One borrower file from application through closing, servicing, and review — and a new loan program deployed as a configuration, not a build.

Source-cited AIReview- and examiner-readyLive in 60 days

- $1.5B+

- Active program-credit deals

- 50+

- Deals currently underwriting

- 60 days

- Typical live window

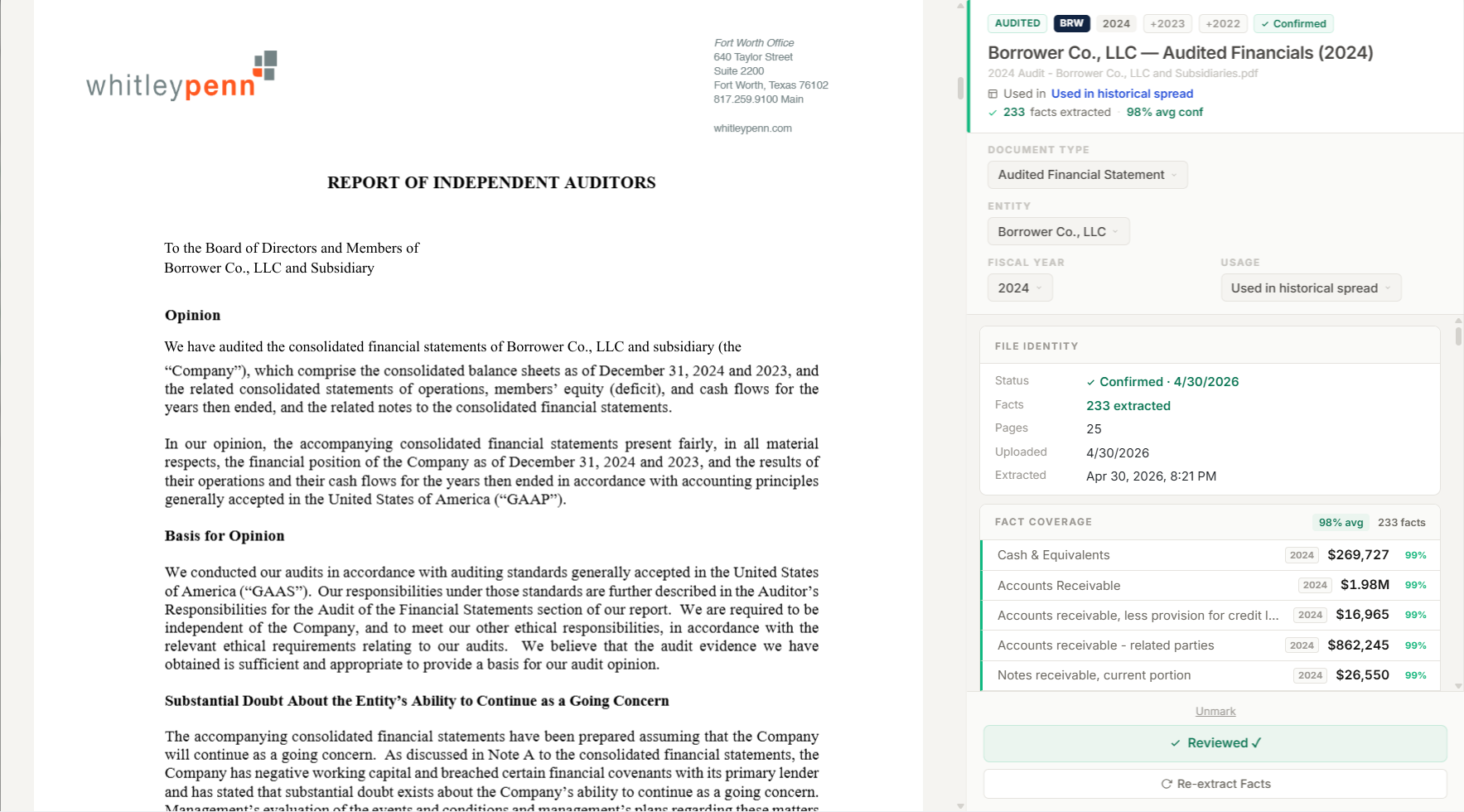

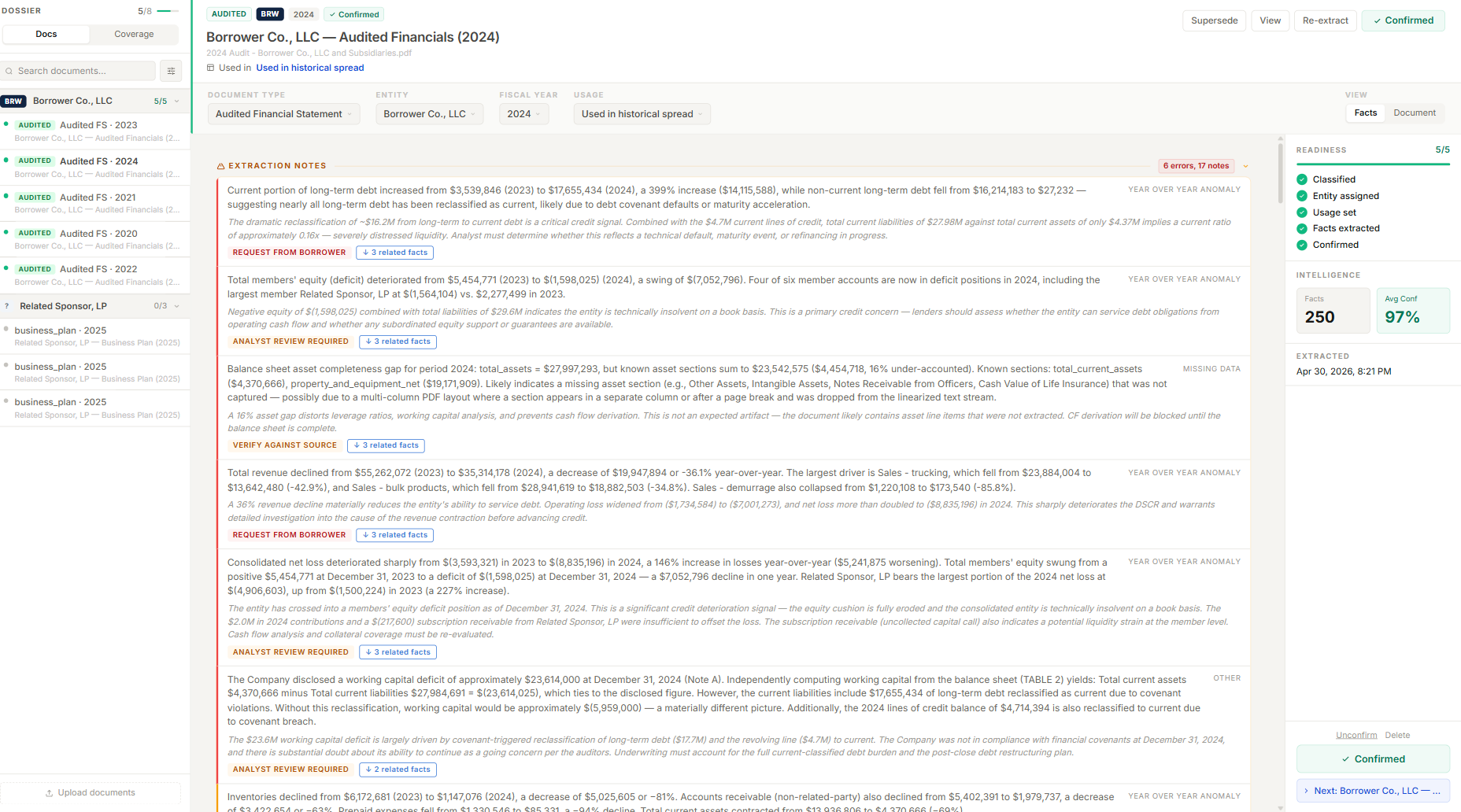

§ Product proof · Source to audit

From source evidence togoverned credit judgment.

Real, redacted product surfaces. The source document, extracted fact, analyst decision, and audit event stay in the same borrower file.

The model flags what a credit officer would investigate.

Every decision lands in the event log with evidence attached.

MORE CAPTURED SURFACESINTAKE INBOXSPREADING + REVIEW DRAWERDEAL-FILE SEARCHCOVERAGE MAPView the platform

§ Programs · Supported

Built for the lenders other vendors call “edge cases.”

01

CDC

SBA 504

02

Farm Credit

FCS Title I & III

03

USDA

B&I · CF · REAP · Rural

04

HUD

232 · 223(f) · 221(d)(4)

05

EB-5

Regional Centers

06

C-PACE

Energy · Water · Resil.

07

CDFI

Cert. CDFI lenders

08

Private Credit

Bridge · ABL · Direct

§ The Engine · Program Studio

One underwriting engine.

Every program is a configuration.

Plenty of software moves the file. CORE underwrites it — then carries the decision through closing, servicing, committee review, diligence, and examination without rebuilding the platform around each program.

FIGURE · CORE ARCHITECTUREEvery program family · one engine · one audit trail

SBA 504

USDA B&I

HUD 232

EB-5

C-PACE

CDFI

Farm Credit

Private Credit

Every program family. One engine. One audit trail.

Your document list.

Collection packages — base plus add-ons — not a hardcoded checklist.

Your credit box.

Underwriting policies built from your own metric, covenant, and scorecard catalogs — versioned, assigned per program, switchable mid-deal when the lender or capital source changes.

Your memo.

Templates define sections, intents, and mandates. There is no fixed memo.

Your industry research.

COREView reports generate from configurable profiles — the same discipline as the memos.

PIPELINE · ROLLING WINDOWSOURCE · CORE PROJECT ACTIVITY

$1.5B+across50+active commercial-credit deals currently underwriting on CORE

C-PACE energy + resiliencyUSDA B&I + REAPEB-5 regional center capitalHUD bridge-to-perm housingBRIDGE interim capital

§ Who We Serve

The segments we serve in depth. One connected decision trail.

One engine, configured by program — packaging, decision, and replay surfaces tuned to each program’s eligibility, review posture, and capital path.

CDCs

504 packaging, eligibility, and credit memo — built against real SBA examination findings.

View CDC buildFarm Credit

Cooperative lending against patronage, captive book, and FCA examination.

View Farm Credit buildUSDA

B&I, Community Facilities, REAP — rural mission, federal scrutiny.

View USDA buildC-PACE

Energy, water, resiliency capital — long-term assessment-backed credit.

View C-PACE buildCDFI

Mission lending with cert-level reporting and donor-defensible files.

View CDFI buildPrivate Lenders

Bridge, ABL, and direct lending — bespoke programs as configurations, files ready for LP and capital-partner diligence.

View Private Credit build§ Platform

Six products on one borrower file.

Find, manage, underwrite, configure, close, and service. Most teams land in Workflow or Underwriting, then add products as the operation is ready.

01Find

CORE Lead Discovery

Program-fit borrowers

Find borrower opportunities that fit your programs - human-screened before they touch the pipeline.02ManageCORE Workflow

Manage the file

Manage the borrower file: pipeline, portal, collection, data room, routing, and audit trail.Most teams land here03UnderwriteCORE Underwriting

Underwrite the deal

Underwrite the deal: Table Evidence, spreads, pro forma, capital, coverage, risk, and COREView.Most teams land here04ConfigureCORE Programs

Configure each program

Program-specific credit memo analysis - grounded in evidence, policy, risk, and analyst review.Human-in-the-loop05CloseCORE Closing

Close with control

Close with control: approval snapshot, conditions, funding reconciliation, blockers, and human certification.06ServiceCORE Servicing

Service the portfolio

Service the portfolio: boarding, obligations, ledger, payment controls, reviews, and action packages.Six products on one borrower file. Most teams begin with Workflow or Underwriting, then add products upstream or downstream as the operation is ready.

Configured by Program Studio

A loan program is a configuration, not a build.

Collection packages, underwriting policies, and memo templates stay versioned by program.

§ AI · Built for examination

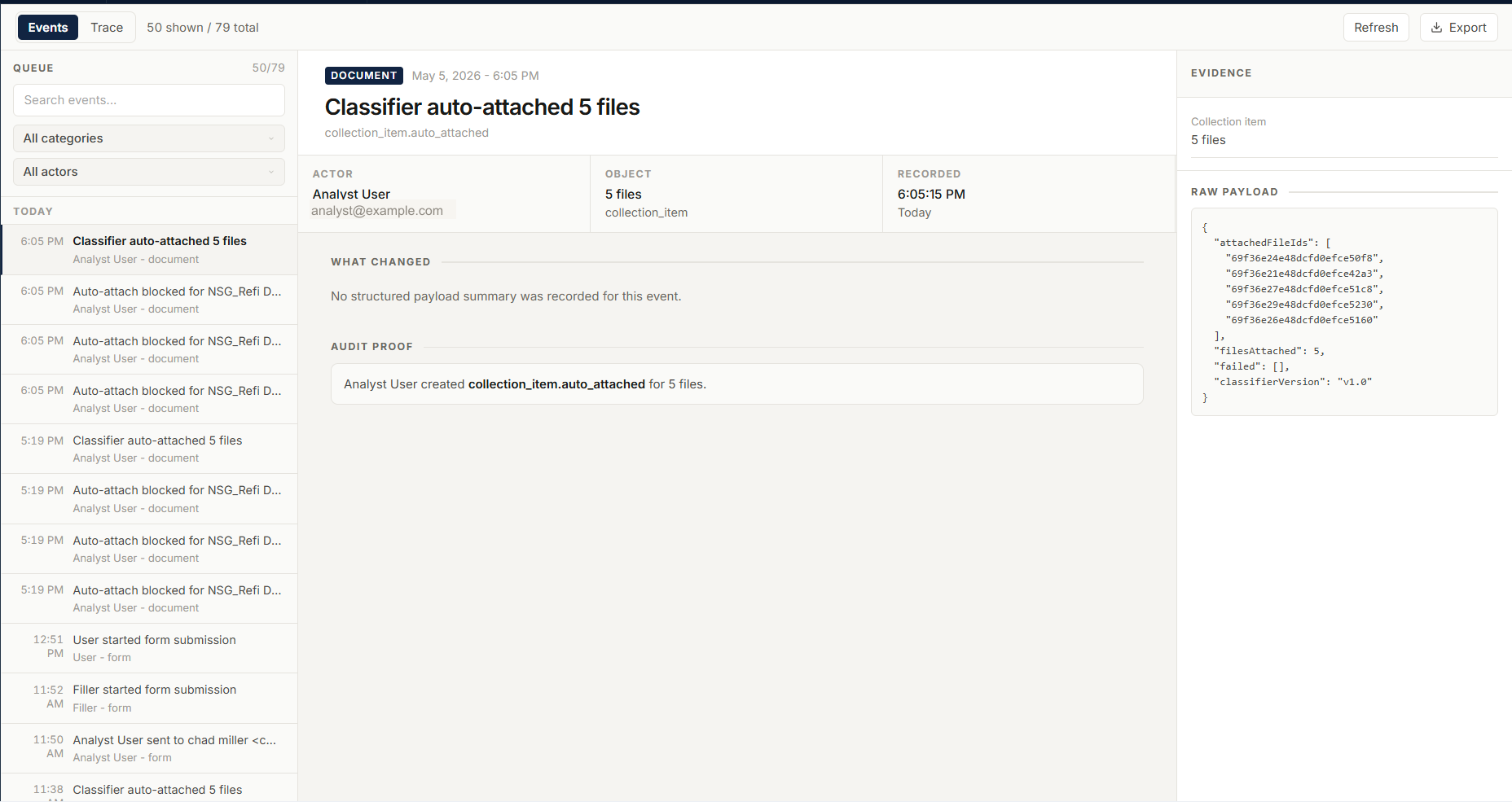

AI in CORE is judged by its citations, not its prose.

These controls answer the question credit teams get after the memo is written: where did this claim come from?

- Cite-or-decline. If the model cannot ground a claim in a file, rule, or accepted fact, it declines to write it.

- Analyst-owned decisions. The model proposes; the analyst accepts, edits, or rejects. The human decision is logged separately.

- Audit-ready snapshots. Model, inputs, output, and overrides are frozen against the loan file — replayable after the decision.

- The receipt. The analyst assembles the evidence; the receipt proves what the model saw.

- Organized like a credit department. 23 personas across four divisions — underwriting, credit policy, program policy, operations — route section work to analyst-and-supervisor pairs per program. Every agent action is timestamped, actor-named, and queryable.

decisionFILE PINNED · Tax Return — 2023

modelclaude-sonnet-4-6 · 2026-03-19

skillcredit-analysis-spreading@v3.2.1

candidatesMercerMfg_2023_1120S.pdf · conf 0.94 · PINNED

MercerMfg_2023_K1.pdf · conf 0.81

MercerMfg_2023_K1.pdf · conf 0.81

analystR. Tabori · approved · 14:22:11 EDT

snapshot3f9c-b21e-44a7-c019

§ Origin · Built in production

Built inside a working commercial-credit shop. Against real examination findings. While the loans were closing.

Every major surface came from pressure inside the work: analysts assembling files, supervisors checking memos, lenders answering examination questions, borrowers waiting on decisions.

SBA, USDA, and conventional bridge are the configurations Waterside runs on its own deals — the product is used on the builder’s book before it is sold.

§ COREView · Live library

Public industry credit intelligence.

§ Request demo

Pick the path that matches your program.

Demos are 30 minutes — real deal artifacts, source citations, and the audit trail behind a credit decision. Bring your hardest credit-review question.

- CDCI run a CDC

- FCSI work at Farm Credit

- USDAI originate USDA loans

- PRIVI run a private credit shop

- PILOTSend us a dead deal — we'll run it through CORE

Source-cited AI · Human-controlled decisions · Review-ready replay · Live in 60 days