Impact does not replace credit

The strongest files prove repayment, purpose, borrower context, and mission relevance together.

§ Who We Serve - CDFIs

CDFI files carry two obligations at once: make a sound credit decision and preserve the borrower, community, funder, and impact context that explains why the capital matters.

CORE is a fit when CDFI underwriting needs repeatability, source control, funder diligence, board-ready packages, or investor review without reducing the borrower to a generic credit memo. Fund-specific underwriting lives as your own policy and memo template - mission context included, nothing hardcoded.

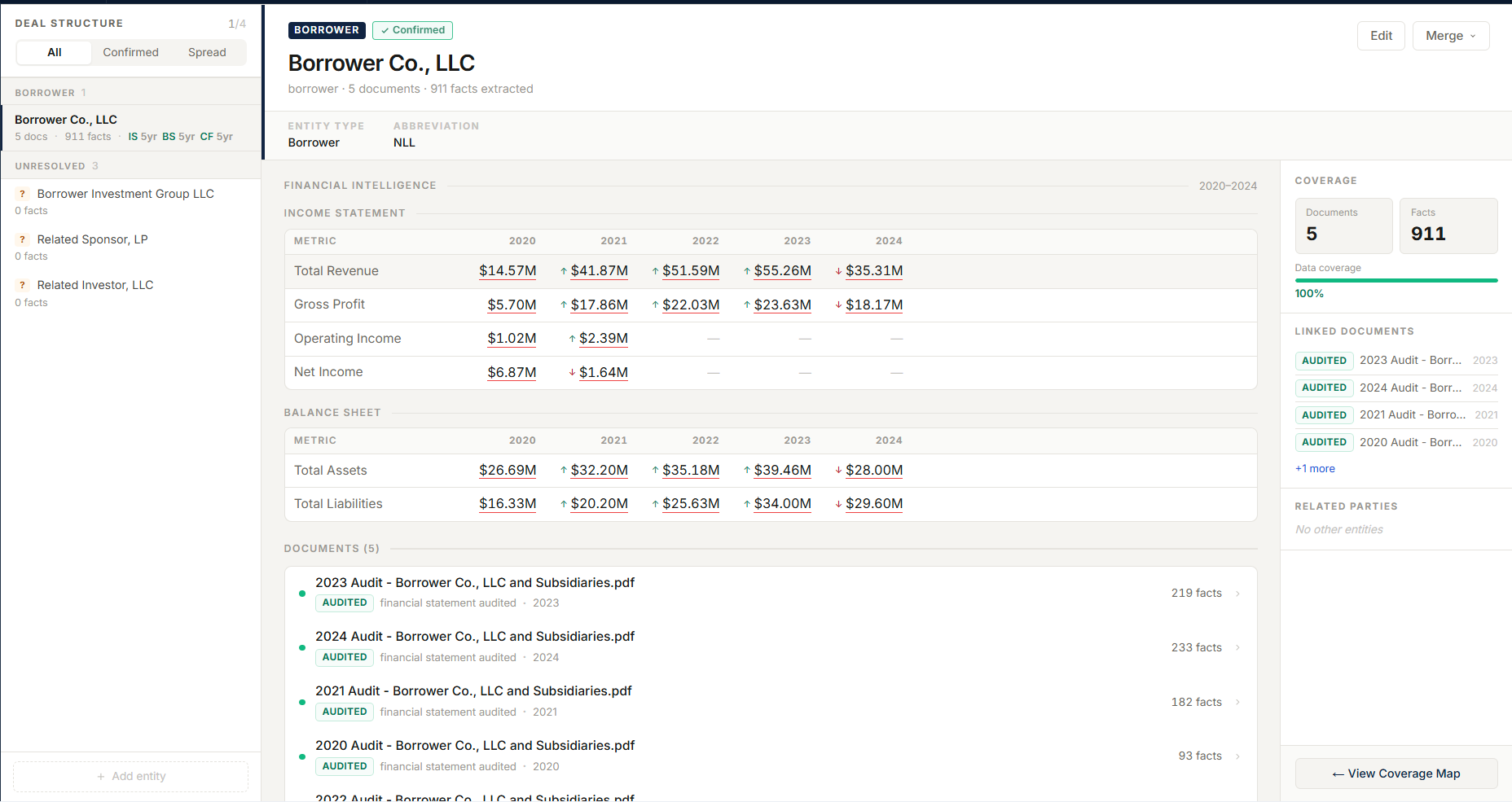

Borrower facts, financial intelligence, and source lineage§ Mission Credit

The strongest files prove repayment, purpose, borrower context, and mission relevance together.

TA notes, requested documents, revised financials, borrower explanations, and diligence context should not disappear before underwriting.

Spreads, adjustments, cash flow, DSCR, and exceptions should resolve back to the borrower source material.

Target market, use of proceeds, geography, impact thesis, and program eligibility should be attached to evidence, not remembered.

Board packets, investor diligence, grant reporting, and portfolio review all need the decision story and the source record.

CORE helps turn one-off mission-credit judgment into a controlled workflow without stripping out local context.

§ Fit

This is an adjacent fit where evidence control and repeatable underwriting matter more than generic CRM automation.

Borrower intake, document collection, and technical-assistance context

Financial spreading with source facts, adjustments, and exception notes

Impact, target-market, eligibility, and use-of-proceeds evidence organization

Board, funder, investor, or grant diligence package support

Analyst-owned memo support and review history

Audit trail for source documents, decisions, and package updates

§ Path

Start where underwriting evidence, mission context, and funder reporting pressure overlap.

Map documents, facts, TA context, review stages, impact evidence, and decision ownership.

Use an active or anonymized borrower file to compare spreading, memo support, package review, and diligence output.

Keep the first deployment focused on measurable credit, diligence, and reporting lift.

§ In Depth

A CDFI credit file has two audiences with different questions: the credit side (repayment, collateral, coverage) and the funder side (impact, compliance with funding covenants, board and grantor reporting). Generic loan software flattens the second audience into a notes field. CORE lets mission context, funder diligence requirements, and impact documentation live as first-class collection and reporting requirements in the same borrower file as the credit work — one record that answers both audiences.

CDFIs run lean, but their reporting obligations — federal funders, foundations, aggregators, board committees — are institutional-grade. The leverage is in infrastructure that produces the defensible record as a byproduct of doing the work: source-cited analysis, policy evaluation against the CDFI's own credit box, and replayable history, without a dedicated back-office team maintaining it.

CDFI lending follows funding: a new allocation, a new program, a new geography. Because CORE treats each loan program as a configuration — collection package, policy, memo template — a CDFI can stand up the new program's workflow without an engineering project, and retire it just as cleanly.

§ Next Step

We will help decide whether CORE belongs in the underwriting file, the diligence file, or the board package workflow.