SBA 504 packagers

Package borrower files, eligibility, debenture timing, closing conditions, and SBA-ready evidence without spreadsheet sprawl.

§ Who We Serve

CORE is built for commercial credit teams whose programs, policies, borrower structures, and diligence obligations do not fit a generic loan workflow. Public-program lenders, relationship lenders, mission lenders, and private credit teams all configure the same engine around their own credit work.

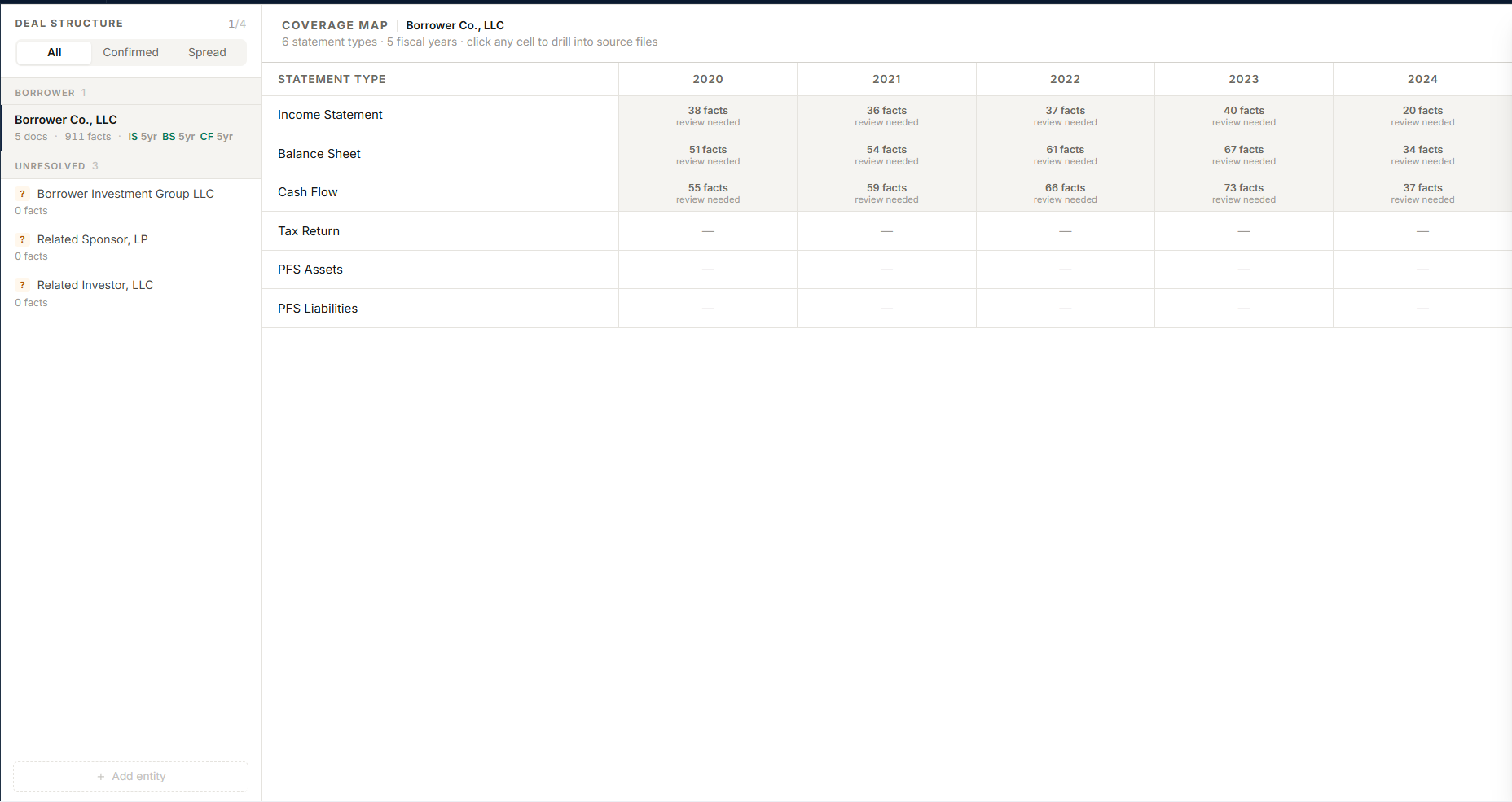

CDC, Farm Credit, USDA, C-PACE, CDFI, and private credit teams all need to prove how a decision was reached. CORE keeps the borrower file, source evidence, policy state, analyst actions, and audit trail together while each team configures its own program.

Program views inherit one audit trail§ Credit Environments

Package borrower files, eligibility, debenture timing, closing conditions, and SBA-ready evidence without spreadsheet sprawl.

Route cooperative credit work through documented policy, collateral, borrower financials, and FCA-grade examination posture.

Handle OneRD, B&I, REAP, and community-facility complexity with source-cited credit analysis and reusable program logic.

Keep property evidence, eligible measures, lender consent, program rules, closing conditions, and assessment history in one controlled record.

Preserve repayment evidence, mission context, impact support, funder diligence, and board review without flattening the borrower story.

Run bridge, ABL, and direct-lending strategies as configured credit programs with diligence-ready files for committees, LPs, and capital partners.

§ Fit

The strongest fit is a lender or operator with repeatable, document-heavy credit work and a real obligation to explain the decision later.

Program-specific underwriting and packaging

Borrower collection, file matching, and document intake

Analyst-controlled AI with source citations

Memo support, audit replay, and event-level history

§ Path

Packaging, eligibility, closing checklists, and SBA-ready file control.

Policy, borrower financials, collateral, and examination discipline.

B&I, CF, REAP, and rural credit files with rule-bound underwriting.

Eligibility, lender consent, project evidence, and recorded assessments.

Credit discipline, impact context, funder diligence, and board-ready evidence.

Bridge, ABL, and direct-lending credit boxes configured for committee and investor diligence.

§ In Depth

A CDC's 504 package, a Farm Credit association's cooperative file, a USDA lender's B&I project, a C-PACE administrator's assessment record, a CDFI's dual credit-and-mission file, and a private credit fund's diligence-grade record are different work products — but they are built from the same spine: controlled collection, source-linked evidence, the lender's own policy, recorded risk decisions, and memo output the team configures. The segment pages below carry the specifics for each operation.

§ Next Step

We will show where CORE fits, where it does not, and what would need to be configured before launch.