Where do the rules live?

Can the platform hold the program's governing material - SBA SOPs, USDA regulations - as dated, citable sources inside the underwriting, or does program knowledge stay in a veteran's head?

§ Compare - For SBA & USDA Program Lenders

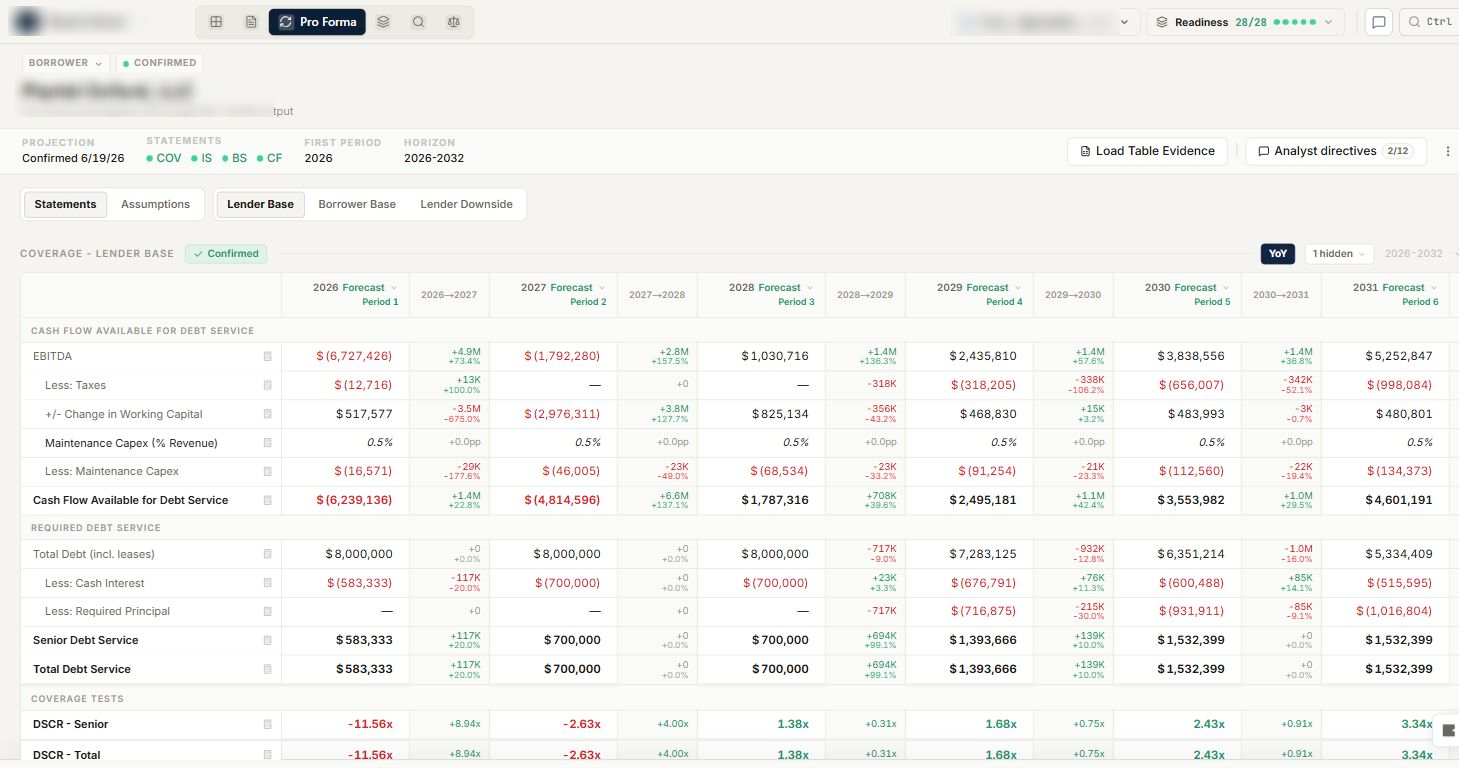

Most SBA lending software is built as a volume factory: standardized intake, forms automation, throughput. Program lenders live on the deals that are not standardized — and those deals stall in the judgment work, where intake software does not reach.

Multi-entity borrowers, projections-dependent B&I projects, eligibility interpretation, structuring constraints from the SOP and CFR: complex program deals are decided in the underwriting layer. Compare platforms on where that work actually happens.

Comparison pages use careful factual claims§ What To Compare

Can the platform hold the program's governing material - SBA SOPs, USDA regulations - as dated, citable sources inside the underwriting, or does program knowledge stay in a veteran's head?

A program-configured policy with your thresholds, covenants, and scorecards - or a generic checklist with the program's name on it.

The memo should carry recorded underwriting decisions and citations an agency reviewer can follow, not re-derive conclusions at drafting time.

7(a), 504, and B&I should run as configurations of the same engine - not as three vendors and three files.

§ Fit

CORE is not competing to win the standardized-intake race; it owns the underwriting and evidence layer where complex program deals are decided.

Program-specific collection packages, policies, and memo templates

Governing regulations integrated as dated, citable source libraries

Projections, capital stack, and coverage built for guaranteed structures

Cited industry credit analysis by program (COREView)

Records that anticipate agency and examiner review

§ Path

Intake and pipeline tooling that already moves standardized files can stay.

Complex files enter CORE for collection, spreading, underwriting, and memo work.

7(a), 504, B&I, and conventional programs deploy as configurations, not projects.

The lifecycle grows into closing and servicing as the operation is ready.

§ Next Step

We will walk the file through collection, underwriting, and memo work against your program's actual rules.