The staffing paradox

Institutions building commercial or government-guaranteed capacity need large-bank analysis discipline without a large-bank analyst bench.

§ Compare - For Community Banks & Credit Unions

Community banks and commercial-growth credit unions run on established cores and LOS platforms that are genuinely hard to replace - and mostly should not be. The gap is what happens between intake and decision: spreads in workbooks, memos in Word, policy in a PDF, evidence in email.

Complex commercial deals slow down in the analysis, policy, and evidence work. CORE deploys beside the existing core and LOS, owns that layer, and exports clean records to the systems the institution already trusts.

Comparison pages use careful factual claims§ What To Compare

Institutions building commercial or government-guaranteed capacity need large-bank analysis discipline without a large-bank analyst bench.

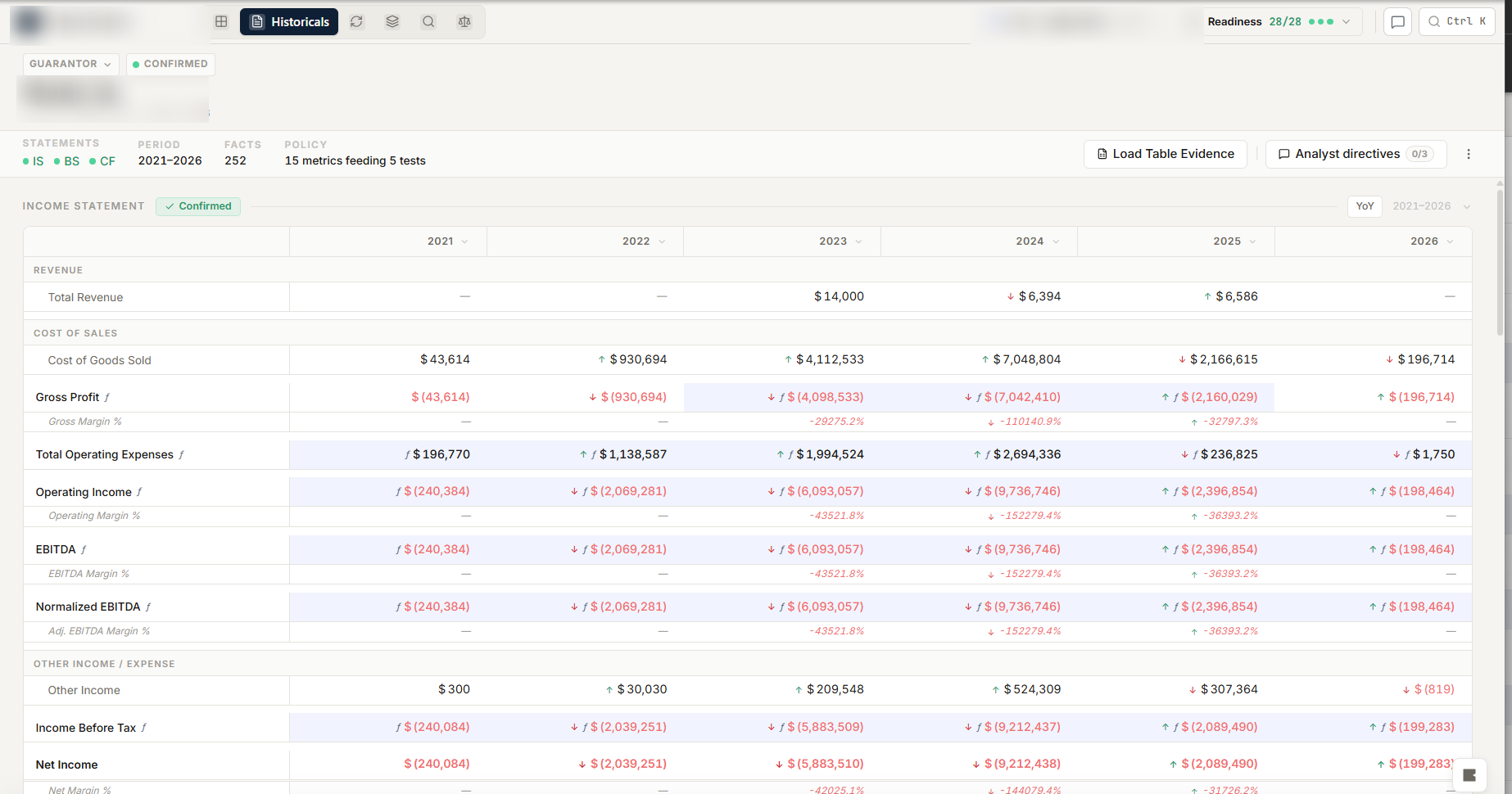

Spreading, policy evaluation, evidence, and memo drafting carried under human control changes what a three-person credit team can produce.

CORE owns the borrower file's underwriting and evidence work and hands records downstream - adoption is a program and a team, not a conversion project.

Source-cited analysis, human approval records, and replayable history support examiners, committees, and model-risk review alike.

§ Fit

No core conversion, no LOS displacement: the judgment layer deploys as its own workspace on the borrower file.

Financial spreading with document authority and analyst confirmation

The institution's own credit policy as versioned configuration

Underwriting workspace for complex and multi-entity commercial deals

Program configurations for first SBA or USDA lending programs

Memo generation under cite-or-decline and human review

§ Path

Start with the commercial or government-guaranteed program where deals slow down most.

Policies, collection packages, and memo structure deploy as the institution's own configuration.

The credit team underwrites live deals in CORE while intake and core systems stay untouched.

Approved records flow to the existing systems the institution already trusts.

§ Next Step

We will show the judgment layer working beside the systems you already run.